When looking at operating expenses on a property, you have both controllable expenses and non-controllable expenses. Controllable expenses are things like repairs and maintenance, property management fees and other expenses that you can have most authority over. On the other hand, expenses like Taxes and Insurance are based on outside factors, like a county assessor or an insurance company writing the policy.

Whenever a property sale occurs, the county tax assessors office will be notified, and they will track what the purchase price is, and slap a new tax bill on the property, based on the purchase price and tax rate.

How do I find out what my property taxes will be?

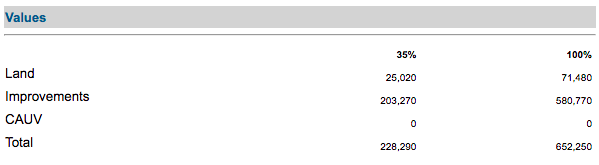

Every county has a property website, where you can search up your specific property by address or parcel number, and it will give you specifics on the property you are looking to purchase. Usually, there will be a “market value” and a “assessed value”. In the state of Ohio, for example, the assessed value is 35% of the market value, and the market value is usually equal to your purchase price (this would be the safe way to underwrite)

Once you know the assessed value, you will see the tax amount. (pictured below)

In order to figure out your tax rate, divide the total tax amount by the market value.

$31,732.06 $652,250 = 4.865015%

Why does a reassessment matter?

The biggest reason a reassessment is vital to understand is because it directly affects your overall return on your deal.

Let’s take a look at an example of a deal largely affected by a reassessment.

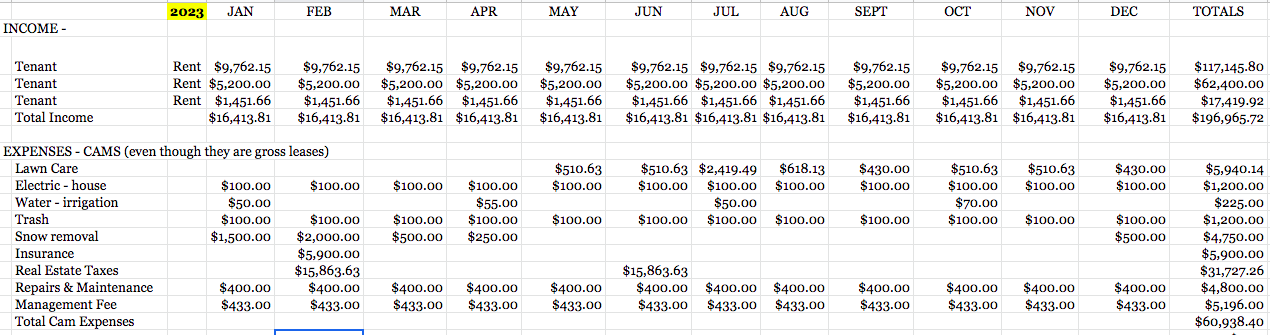

I received this excel sheet from a broker about a multi tenant medical office building in the midwest.

I took everything and began underwriting the deal. I came to a purchase price of $1,300,000 (7.6% cap on their budgeted numbers)

However, when I began looking into their budgeting expenses, I noticed that the taxes they were currently paying were based on the property having a market value of $652,000. (mentioned above)

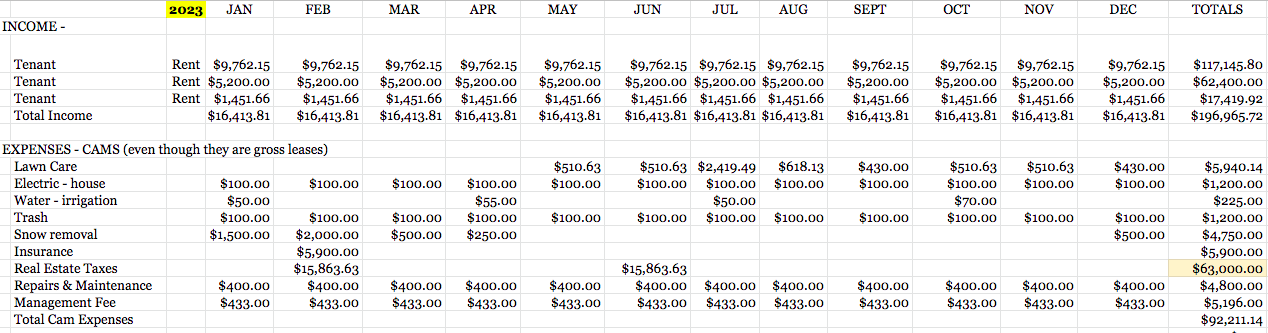

Taking into account the tax rate we came to earlier, I took 4.865015% and multiplied it by my anticipated purchase price of $1,300,000. This resulted in a tax bill of ~$63,246. My taxes would DOUBLE!

This would result in a 15% decrease in my NOI. Ultimately, what I noticed happened was that the building had been sitting vacant for a bit, and the assessor took into consideration the lack of income the building was producing, and lowered the market value of the asset. Now, however, because I would be buying a fully occupied property, the market value would, in fact increase, leading to a much larger tax bill than the previous owner was paying.

While a broker or owner may mean well by sending you the owners historical financials, you must do your own due diligence to understand that the price they paid for the property will be different than what you pay, and will ultimately impact your bottom line. Be sure to consult with local investors, brokers and attorneys on these issues before it’s too late!

Disclaimer: I am not a tax consultant or attorney and do not claim to be one. Please advise on a specified basis with your attorney or tax advisor